MSM Property Quarterly Newsletter Q2: Up by 9.2% year-to-date!

We follow up on our previous newsletter with a summary of the exciting events for the second quarter that maintained listed property as the top performing asset class for the last 10 months. Zinhle Simelane, our listed property analyst, covers the events of the second quarter.

This will be posted on our app for the mobile version. To get the latest information regarding property minute by minute, please follow us on Twitter (@MSMProperty) and for property in all of its form, follow us on Instagram (@msmproperty)

The Listed Property Review for Q2 2024

Introduction

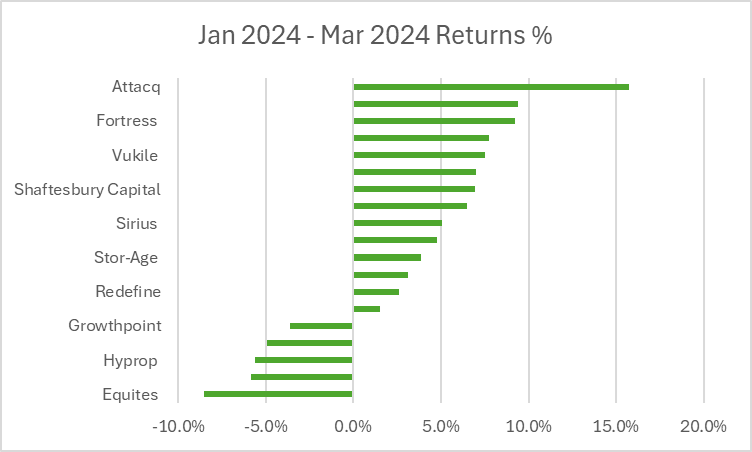

The second quarter of 2024 has proven to be a defining period for South African Listed Property, as it continues to outperform amidst global economic uncertainty. Building on its strong performance in Q1 2024, the sector continued its upward momentum in Q2, with the FTSE/JSE All Property Index (ALPI) delivering a 5.7% return. Notably, the ALPI has achieved a 9.2% year-to-date gain, positioning it as the top-performing domestic asset class on the JSE. Moreover, SA property was ahead of major global indices in Q2, including global property which was down -1.7% in USD, as well as both emerging markets and global world equities which were up 4% and 2.6%, respectively.

Performance Overview

Similar to Q1, the second quarter of 2024 was shaped by a complex mix of economic indicators, such as persistent inflationary pressure and high interest rates, along with geopolitical developments in the Middle East, shaping a diverse landscape for global markets. Despite these challenges, South African equities demonstrated robust performance during this period. SA equities, as measured by the FTSE/JSE All Share Index (ALSI), returned 8.2% in Q2, driven by the Financials (+17.1%), Resources (+4.8%) and Property (+5.5%) segments.

In June, South Africa, along with the United States and Japan, stood out for robust market performance, contrasting with the more subdued or negative returns in Europe and China. The U.S. markets showed resilience, with the Nasdaq and S&P 500 posting significant gains driven by optimism around artificial intelligence and strong performances in technology stocks. The Federal Reserve’s decision to hold interest rates steady in June kept speculation about future monetary easing alive. Meanwhile, European markets, particularly in Germany and France, faced headwinds due to political uncertainty and economic slowdowns. China’s market struggles persisted (initially caused by the bust in the property sector), hampered by concerns over economic recovery and geopolitical tensions. Japan, however, posted solid gains, benefiting from stable inflation and economic policies. These global comparisons highlight the resilience of the South African market in the face of international economic headwinds, underscoring its appeal to both local and global investors.

SA’s market performance in Q2 2024 notably surged towards the latter part of the quarter, driven by sentiments around the National and Provincial Elections (NPEs) in May and the subsequent conclusion of the new South African government in June. Despite market expectations that the leading party, African National Congress (ANC), would secure a much higher vote share which would enable them to form a coalition with smaller parties, the ANC received only 40.2% of the voter count. This unexpected outcome was seen as a pivotal moment for South Africa’s political landscape, leading to the formation of a new Government of National Unity (GNU).

Figure 2: The new government of national unity (GNU) cabinet, source: South African Presidency.

The Johannesburg Stock Exchange (JSE) benefited from the political stability brought about by the GNU, comprising the ANC and nine other parties, formed after two weeks of intense negotiations. This coalition was seen as a market-friendly development, fostering perceptions of continuity in economic and government policies while emphasizing accountability and transparency. This outcome contributed to the strengthening of the Rand, which appreciated by approximately 3.3% against the US Dollar in June, ending the first half of 2024 as one of the few major currencies to appreciate against the Dollar year-to-date. However, this strength in the local currency negatively impacted JSE-listed stocks with foreign earnings.

The South African Reserve Bank (SARB) maintained the base lending rate at 8.25% for the quarter, reflecting its strong focus on curbing inflation. May’s CPI remained at 5.2% y/y, barely lower than the 5.3% y/y at the start of the year, and still well above the target of 4.5%, highlighting persistent inflationary pressures. Even with some relief from reduced load-shedding, the economy showed little improvement, with Q1 2024 GDP growth dipping slightly to -0.1% from a revised 0.3% in Q4 2023. Nonetheless, the SARB stood by its growth predictions of 1.2% for 2024 and 1.3% for 2025.

Sectoral Insights

Retail Sector

The retail property sector in South Africa showed resilience during the second quarter of 2024 despite ongoing economic challenges. The MSCI South Africa Quarterly Retail Trading Density Index reported an annualized trading density of R41,053 per square meter for the year ending March 2024, reflecting a 6.2% year-on-year growth. This growth is notable given the high inflation, elevated interest rates, and unemployment rates impacting consumer disposable income. However, reduced load-shedding and improved sentiment kept consumers visiting shopping centers. Foot traffic in major shopping malls increased in the first quarter of 2024, though spending did not match the rise in visitor numbers.

Vacancy rates in retail properties decreased to 4.4% by March 2024, indicating recovery and stability. Smaller regional centers (25,000-50,000 square meters) saw vacancy rates fall from 5.8% to 5.1%, while community shopping centers experienced slight upward pressure since November. Larger formats like regional and super regional shopping centers exhibited mixed performance, maintaining vacancy rates lower than the peaks of 2021 and 2022 but showing some deterioration since December 2023. Retailers’ cost of occupancy improved as sales growth outpaced rental growth, making the sector more attractive for investment. The retail property sector’s resilience, amid economic challenges, suggests potential growth, particularly if interest rates decrease and retirement fund proceeds support consumer spending.

Figure 3: retail vacancy rates, source: SAPOA

Office Sector

In the second quarter of 2024, South Africa’s office property market continued to recover gradually. The SAPOA Office Vacancy Survey reported an overall vacancy rate decline to 14.2%, down 50 basis points from the previous quarter, marking the eighth consecutive quarter of decreasing vacancies. A slight rebound in office asking rents, with a 0.8% increase, indicates a closer alignment of demand and supply, aided by subdued development activity.

Regional disparities remain significant. Johannesburg faced challenges with a 16.9% vacancy rate, while Cape Town maintained the lowest rate at 6.3%, showing resilience and attractiveness to tenants. The high pre-let rate of new developments, such as the Nexus Waterfall project by Attacq, reflects cautious development practices, ensuring occupancy before construction.

Figure 4: Nexus Waterfall construction site, building 2, source: Attacq website

Despite these improvements, the office market still contends with troubled assets, particularly buildings with over 30% vacancy rates. These assets, difficult to fill, can depress rental rates and complicate market dynamics, especially if sold to opportunistic buyers.

Industrial Sector

The industrial property market, particularly within the logistics sector, demonstrated resilience and growth in the second quarter of 2024. Despite rising building costs, strong structural drivers such as supply chain optimization, onshoring, and e-commerce expansion supported the sector. Rental reversion trends were notable, with Equites Property Fund reporting an anticipated average rental reversion of -18%, reflecting adjustments from historically high rates rather than a market decline. Growthpoint Properties and SA Corporate Real Estate reported improvements in rental reversions, indicating a stabilizing market. Prime market rentals increased from approximately R65/m² to around R85/m², reflecting strong demand and limited supply. The demand for logistics spaces, driven by supply chain needs and e-commerce growth, suggests a healthy and expanding market, pointing to further improvements in market rentals and sector stability.

South African property fundamentals have been navigating a complex economic landscape with varying degrees of resilience and recovery. The retail sector benefits from stable foot traffic and improved occupancy, while the office sector shows gradual recovery with regional disparities. Meanwhile, the industrial sector thrives on strong structural demand. Continued strategic management and adaptation will be crucial for sustained growth and stability across these sectors.

Figure 5: Eastport Logistics Park, source: Fortress Fund Website

Investment Insights: How Bond Yields Influence Property Valuations

Have you ever wondered how the rise and fall of bond yields can affect the value of property investments? in this section, we’ll break down this relationship, helping you make more informed decisions. The bond ad property markets are closely linked, offering investors unique opportunities to balance income and risk. Understanding how bond yields influence property valuations is crucial for making informed investment choices.

Government bond yields, representing the risk-free rate, serve as a benchmark for the returns expected from the least risky assets. Consequently, for riskier investments like listed property, investors demand returns that exceed the risk-free rate to account for risks such as tenant risk, leverage, and capital allocation. In recent years, as interest rates have risen, bond yields have increased, enhancing their appeal and putting pressure on riskier assets like listed property.

Figure 6: The Union Buildings, Pretoria, source: South African Presidency

For South African investors, understanding these dynamics is critical. Recently, South African bonds faced challenges due to the economic downturn following the COVID-19 pandemic, and bond yields rose as a result of increased government borrowing. Yields were also impacted by rising interest rates, geopolitical issues, and a worsening trade balance, all of which eroded investor confidence. Despite these challenges, South African government bonds included a significant risk premium, pushing yields higher. After peaking at 12.8% in April, long bond yields rallied toward the quarter’s end, falling 81 basis points to 11.2%, driven by optimism around the multi-party coalition and a global rally.

Given the attractive starting yields on bonds both locally and globally, we expect the property market to benefit from potentially decreasing yields as we transition into a lower interest rate environment. South African investors should remain vigilant, as understanding and anticipating these yield dynamics will be key to making informed property investment decisions in the coming months.

Outlook

The strong performance of the South African listed property sector in Q2 2024, highlighted by a 5.7% increase in the FTSE/JSE All Property Index (ALPI), underscores the sector’s resilience and growth potential. This outperformance, coupled with a 9.4% year-to-date gain, positions listed property as a leading asset class within the domestic market, outperforming both global property indices and broader equities.

As we look ahead to Q3 and the remainder of 2024, the sector seems poised for continued growth. Property fundamentals are showing improvement. The formation of a Government of National Unity (GNU) and the stabilization of the political landscape have bolstered investor confidence, contributing to a strengthening Rand and positive market sentiment. The anticipated transition into a lower interest rate environment further supports our positive outlook, as decreasing yields are likely to enhance the attractiveness of property investments compared to other asset classes and strengthen valuations.

In conclusion, while the South African listed property sector is well-positioned for continued success, as investors we will remain mindful of potential market volatility due to upcoming geopolitical events, including the U.S. elections. Nonetheless, the sector’s strong fundamentals and strategic developments support a positive outlook for the remainder of the year. Given the current market conditions, investors may want to consider increasing their exposure to listed property, taking advantage of the sector’s resilience and growth potential. We maintain a positive sentiment towards this asset class, anticipating further gains as the year progresses.

We ask you to be safe and feel free to contact us with any questions and we appreciate your support and confidence in us, in being able to manage your wealth.

Zinhle Busisiwe Simelane is an integral part of our team at MSM Property Fund, serving as the Listed Property Analyst. With a solid foundation established as an Asset Management Intern at Emira Property Fund, she refined her skills in research and analysis. Transitioning to Afrifocus Securities, Zinhle excelled as an Equity Research Analyst, specializing in JSE-listed property companies. Armed with a BSc in Property Studies from the University of Witwatersrand and currently in pursuit to be a Chartered Financial Analyst (CFA) Charterholder as a CFA Level 2 candidate, Zinhle’s dedication to excellence is evident. Her expertise enhances our capabilities in constructing our portfolio, driving us toward continued success in the property investment landscape.