|

DEAR INVESTOR, We break our silence with a quarterly update on listed property as it was the best listed asset class on the Johannesburg Stock Exchange in 2023 with just over 10% in total return perspective. Zinhle Simelane, our listed property analyst, covers the first quarter and the sectors prospects. This will be posted on our app for the mobile version. To get the latest information regarding property minute by minute, please follow us on Twitter (@MSMProperty) and for property in all of its form, follow us on Instagram (@msmproperty) The Listed Property Review for Q1 2024 Introduction In the first quarter of 2024 the growth of the property market slowed down compared to the strong performance we saw from November 2023 to January 2024. Despite this slowdown, the listed property sector is still doing better than other asset classes so far this year. Listed property performance, shown by the JSE All Property Index (ALPI), went up by 3.5%. On the other hand, the JSE All Share Index (ALSI) dropped by -2.2%, the JSE All Bond Index (ALBI) dropped by -1.9%, and cash investments increased by 2.1% in Q1 2024. However, the good news were dampened by some negative changes we saw, especially in March. During that time, the property market returns went down by -0.6%. This might be because investors started thinking differently about whether interest rates would go down soon and also because of how well property companies did in their financial reports for the first quarter of 2024. Some companies, like Growthpoint Properties and Hyprop Property, didn’t do as well. Their distributable income per share (being profits made from rentals) decreased significantly. But companies like Vukile Property and Attacq, which expected to do better in the financial year 2024, saw their share prices go up instead. |

|

| Figure 1: Asset Class Returns In Real Terms; source: Old Mutual Investment Group |

|

Operationally, the commercial real estate sector is getting more stable, but there’s still worry about how much money companies can make due to them spending on finance costs. The markets in general are hoping that the central bank will cut interest rates a lot later this year, which could help ease this pressure. Most businesses are already expecting these rate cuts to happen in the second half of the year. But there are other problems hanging over the property market, especially with the general elections coming up in May in South Africa. If there are big changes in politics, it could make markets more uncertain for policies, especially if there’s a chance of a coalition government or if new parties, like the MK Party led by former president Jacob Zuma, become popular. Furthermore, local challenges such as social unrest, infrastructure deficiencies, and global geopolitical events may hamper growth prospects. Despite this, there is some optimism with loadshedding having subsided in the current year to date and meaningful discussions being had for the restoration of Transnet. These SOEs (state owned entities) have a significant impact on the health of the South African economy to bolster growth and employment. Sustainability is increasingly becoming a focal point in real estate investment decisions. Strategic investments in solar and water assets, coupled with a focus on environmental, social, and governance (ESG) factors, are anticipated to enhance property values over the long term and ensure no interruptions in the short term for their tenants. |

|

| Figure 2: Illustration by Karen Moolman |

|

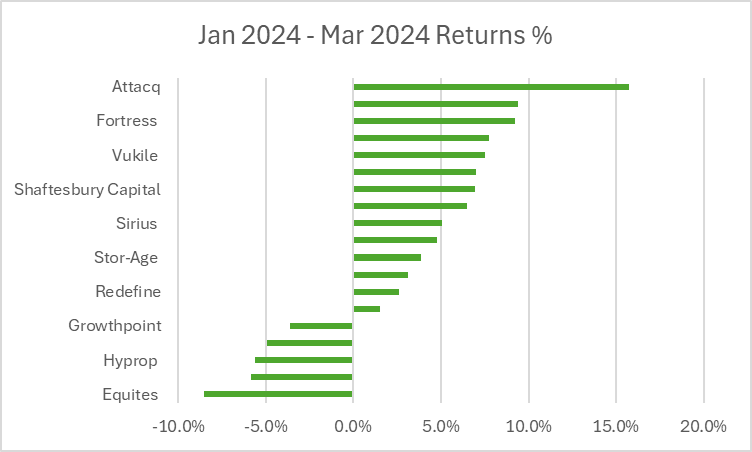

Financial Results at end of April Recent financial results were mixed, influenced notably by economic factors like rising funding costs and constrained liquidity. The distinct differences in performance observed within the listed property sector last year persisted into this year. In the previous year, we saw a prevailing pattern where certain companies, such as Attacq, Fortress, and Shaftesbury Capital, experienced notable growth due to corporate actions such as mergers etc, alongside a resurgence in offshore property companies like London-focused Shaftesbury Capital and European retail property firms, which saw a rebound from the 2022 sell-off. Conversely, South African-based property firms like Growthpoint and Equites faced challenges, reporting negative earnings outlooks attributed to higher financing costs, resulting in underperformance. In the first quarter of 2024, this trend of performance divergence continued, primarily driven by differing outlooks on earnings growth. Companies maintaining a negative outlook on earnings, including Growthpoint (-3.6% in Q1), Equites (-8.5% in Q1), and Hyprop (-5.6% in Q1), saw negative returns. Conversely, companies able to report increased growth expectations and revise earnings guidance upwards due to strong operational performance and effective balance sheet management, such as Attacq (+15.7% in Q1), Vukile (+7.5% in Q1), and Nepi RockCastle (+7.7% in Q1), continued to enjoy positive returns. |

|

| Figure 3: JSE ALPI Returns for Q1 2024, source: IRESS |

|

The recent earnings season showed that the property fundamentals are improving with stabilizing vacancies across subsectors, improving reversions, and valuation write-downs bottoming out offer some cause for optimism. Vacancy rates have decreased across all sectors, with retail and industrial sectors showing significant improvements. Due to muted development activity, the office sector has also experienced an improvement in vacancies, with the vacancy rate down from a peak of 16.7% to 14.7% in Q1 according to SAPOA. Financially, property companies maintain a stable yet relatively high aggregated Loan-to-Value (LTV) ratio, suggesting manageable debt levels despite some decline in asset valuations. The LTV across the sector improved to 39.6% for December 2023 but remains at the upper end of its long-term history. However, in the midst of the macroeconomic and geopolitical landscape, the quality of management teams and portfolios will be the primary driver of performance divergence and will play a crucial role in determining which companies outperform. Sectoral Insights Despite challenges, certain property sectors exhibit resilience and growth potential. However, some subsectors performed better than others. Industrial and neighbourhood retail sectors remain strong performers, driven by factors like e-commerce growth and reshoring trends. In contrast, the office sector continues to face challenges with weak demand, although quality assets in prime locations are expected to fare better. Residential properties, particularly those in municipalities with good infrastructure and security, are expected to benefit from the semigration trend. However, the impact of interest rate changes on the residential sector remains a concern. Retail Sector Recent developments in the retail sector signify a notable turnaround for shopping center owners, who have weathered a difficult period marked by the pandemic, social unrest, and economic strains. This led to retail vacancies reaching a peak of 7.2% in March 2021 as reported by the MSCI South Africa Retail Trading Density Index. To date, there has been significant improvement in the sector, with vacancies dropping to 4.5% in the final quarter of 2023, this decline suggests absorption of excess supply. While the sector is still experiencing signs of oversupply, there has been limited new developments of shopping centres and this will bode well for the sector. The release of encouraging trading metrics by leading real estate investment trusts (REITs) indicates a resurgence in activity, with sales turnover on the rise, foot traffic increasing, and vacancy rates declining across various mall portfolios. Noteworthy performers such as Attacq and Fortress exemplify this trend, showcasing resilience and adaptability in navigating the shifting landscape, with properties like Mall of Africa and Fortress’s diverse non-urban shopping centre holdings demonstrating robust performance amidst challenging circumstances. |

Figure 4: Jabulani Mall, source: Vukile Property Fund Website |

Figure 5: Mall of Africa, source: Attacq Property Fund Website |

|

Additionally, retailers’ expenses for renting or owning their stores were the lowest they’ve been in almost ten years, represented by the cost of occupancy at 6.8% in Q4 2023, according to SAPOA. When these expenses are lower, it means property companies can make more money, draw in more tenants, and do better against their competition. This positive development has been fuelled by robust tenant sales growth outpacing rental growth, resulting in improved occupancy cost ratios and reduced average vacancies. So, because of this, landlords have more power when they’re talking about leasing agreements, which means they can negotiate better deals for themselves. With more landlords achieving better rentals for their retail spaces, it looks like the retail industry is getting better, despite ongoing economic problems. But there’s a twist to this story with Pick ‘n Pay (PnP), one of South Africa’s big food stores, facing difficulties lately. They’re struggling to keep up with other strong competitors in the market and haven’t been investing enough in making customers happy. Because of this, they haven’t been doing as well as their competitors in the last five years. On the other hand, stores like Shoprite have been getting popular because they’re appealing to customers , especially during tough financial times. People are spending less and choosing cheaper brands, which is hurting stores like PnP. This worries landlords who have PnP stores in their buildings, especially after what happened with Edcon’s financial problems impacting the retail sector. |

|

| Figure 6: Pick ‘n Pay store, source: Business Live |

|

While exposure to the retailer could lead to potential outcomes such as lease cancellations, downsizing of retail space, rental concessions, and write-offs of arrears, landlords do not seem too worried about the retailer in their portfolio. This nuanced backdrop underscores the intricate interplay between retail dynamics, consumer behaviour, and the broader economic landscape, shaping the trajectory of mall owners and retailers alike in the South African market and furthers the move towards non-discretionary spend retail which we believe will maintain resilience in a tough economy. Office Sector During the first quarter of 2024, the South African office market continued to confront challenges stemming from the prolonged impact of the COVID-19 pandemic and most recently the low economic growth environment. However, there have been signs of improvement, with SAPOA reporting national vacancies at the end of Q1 20204 being on a downward trend at 14.7% after peaking at 16.7% in 2022. The shift in vacancy rates was largely driven by a combination of the increased take-up in the A-grade office and improvement in the older C-grade offices as a result of some of the vacant offices being converted to residential or other uses. |

|

|

The ongoing evolution of workplace dynamics, including the increasing acceptance of remote or hybrid work models, continued to shape tenant demand, with implications for office space utilization and occupancy levels. But even with these challenges, there are chances for office buildings in great locations with modern features to attract tenants who want flexible and collaborative workspaces. Developers are being careful because business growth and confidence aren’t strong, so they’re not building many new office spaces unless tenants really need them. Also, office rents are staying low, with landlords often not making as much money when leases renew, and overall rents not going up much. We’re not expecting big improvements right away, but there are some signs of hope, like more demand for high-quality spaces and not too many new offices being built, which could make the office market better. Industrial Sector The industrial property sector maintained its resilience throughout the first quarter of 2024, buoyed by a robust combination of factors including the continued expansion of e-commerce, reshoring trends, and limited land supply. These long-term demand drivers, alongside inelastic land availability, contributed to a steady growth trajectory in rental rates. The sector also continues to have the lowest vacancy rates comparably, with the sector having an average of 2.5%. Yet, there are difficulties arising from higher costs to borrow money and having assets that don’t bring in much profit, which might lower the value of industrial properties. But even with these challenges, industrial properties still look attractive to investors because they can generate a lot of cash and there’s good demand for them compared to how many are available in terms of supply. Although concerns about borrowing costs and property values continue, the basic strengths of the industrial sector are still strong, giving investors chances to make steady profits in a changing market. Against this backdrop, the industrial sector, constituting 12% of the MSCI index, sustained its relative outperformance with a commendable return of 11.2% during the period. Low vacancy rates and a surge in tenant-driven developments continued to bolster the sector’s performance, with the logistics sector, part of the industrial sector, is doing especially well because there’s a lot of focus on making supply chains work better and bringing operations closer to home. Also, because of tensions between countries, it’s become even more important for businesses to have safe and modern facilities, which have increased the demand for these spaces. In the future, things look good for the industrial sector because there aren’t many empty buildings, building costs are going up, which might raise rent prices, and there’s still a lot of interest in high-quality properties despite changes in the market. |

|

| Figure 8: Eastport Logistics Park, source: Fortress Fund Website |

|

Alternative Property The South African alternative property sector showcased a mixed performance in the first quarter of 2024, with various subsectors experiencing distinct trends. Despite some difficulties like higher interest rates and inflation, the residential sector stayed strong, especially in places with good infrastructure and safety. People still want to live in residential areas, although there were worries about how interest rate changes might affect the sector later on. Some companies were smart and invested in solar power and water systems to help manage their costs better and follow the trend towards sustainability. Other parts of the alternative property sector, such as storage and data centres, also looked like good places to invest money because more people needed storage and businesses wanted better digital systems. Investments in data centres, for example, were expected to make a lot more money because businesses care a lot about keeping their data safe and having systems that can grow with them. Similarly, self-storage businesses were doing well because people needed flexible storage options. Overall, healthcare, student housing, and data centres were getting a lot of attention from investors because they seemed safer than regular commercial real estate. Healthcare especially looked promising, even though it’s still new and there aren’t many good investment options yet. Getting money for these new kinds of investments could be tricky at first, but as they become more popular, it should get easier to invest directly in them. |

|

| Figure 9: Vantage Data Center Midrand, source: Data Center Dynamics Website |

OutlookLooking ahead to the rest of 2024, there’s cautious hope in South Africa’s property market, especially if interest rates might go down towards the end of the year. The sector seems like a good bet for investors, with expected modest growth in the near future and potentially good returns of 12% to 15% each year in the long run. Preference is directed towards defensively positioned companies in the retail and alternative subsectors, with a geographical inclination towards Central Eastern Europe over Western Europe, highlighting strategic considerations amidst evolving market dynamics. Looking forward, South Africa’s property market seems to be improving slowly, thanks to some positive signs in the economy and in the property industry itself. But there are still big issues, both globally and locally; so, people need to be smart and keep up with what’s happening. Even though there are challenges, such as problems related to environmental, social, and governance issues, and complicated structures, making wise investment choices can help take advantage of properties that are currently undervalued and set investors up for long-term success. As we transition from an era where macroeconomic factors, like government policies, held much importance to one where the performance of individual companies takes center stage, we can expect a shift in the dynamics of the market. This shift will likely manifest in how investments in property shares respond to global events and trends over the course of the year. |

|

We ask you to be safe and feel free to contact us with any questions and we appreciate your support and confidence in us, in being able to manage your wealth. |

|

| Zinhle Busisiwe Simelane is an integral part of our team at MSM Property Fund, serving as the Listed Property Analyst. With a solid foundation established as an Asset Management Intern at Emira Property Fund, she refined her skills in research and analysis. Transitioning to Afrifocus Securities, Zinhle excelled as an Equity Research Analyst, specializing in JSE-listed property companies. Armed with a BSc in Property Studies from the University of Witwatersrand and currently in pursuit to be a Chartered Financial Analyst (CFA) Charterholder as a CFA Level 2 candidate, Zinhle’s dedication to excellence is evident. Her expertise enhances our capabilities in constructing our portfolio, driving us toward continued success in the property investment landscape. |

MSM Property Quarterly Newsletter Q1: Keeping up the momentum from the 2023 rally!

12

Jul